Electrification is without doubt one of the maximum transformative and irreversible traits within the forklift marketplace, writes Maya Xiao, Analysis Supervisor at Have interaction Research. The systemic shift from inside combustion engines (ICE) to electrical powertrains, predominantly lithium-ion (Li-ion) batteries, is basically reshaping the trade’s aggressive dynamics, operational protocols, and environmental affect.

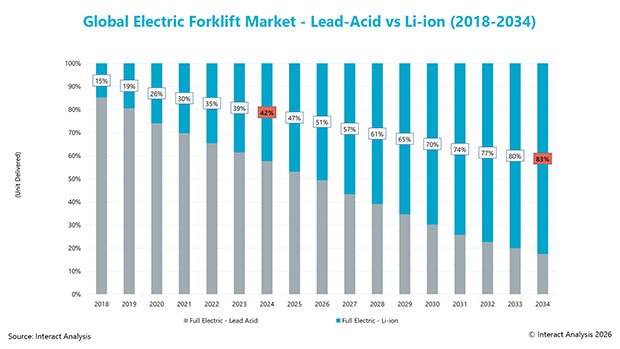

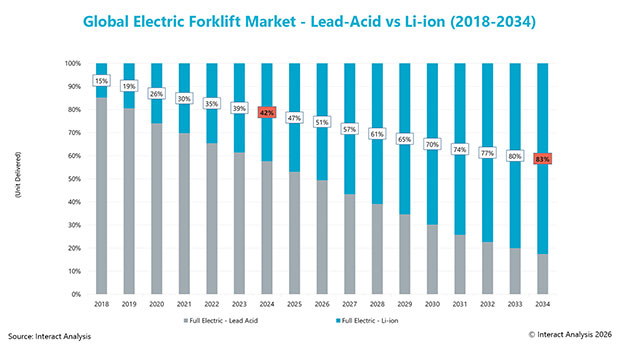

Our lately printed Forklifts – 2025 record charts the meteoric upward thrust of Li-ion forklifts and tasks penetration charges will jump from roughly 32% in 2024 to over 70% via 2034 inside the full-electric sector (which contains Li-ion and Lead-Acid fashions). A pivotal trade inflection level is predicted round 2026, when Li-ion era is forecast to surpass lead-acid batteries in marketplace percentage inside the electrical forklift section.

By way of 2034, a staggering 83% of all new electrical forklifts shipped globally will likely be powered via Li-ion batteries. This speedy transition is overwhelmingly pushed via the compelling operational and financial benefits of Li-ion era.

The trajectory of electrification varies extensively throughout geographical areas, reflecting differing financial constructions, regulatory pressures, and marketplace adulthood.

China is the principle engine of world Li-ion penetration. Its Li-ion forklift shipments are projected to blow up from 26,436 devices in 2018 to over 1 million devices yearly via 2034.

Europe is advancing swiftly, pushed via stringent emissions requirements and robust company ESG mandates.

North The united states lags considerably in the back of, with the United States now not anticipated to succeed in 50% Li-ion penetration till 2032.

Regardless of the transparent expansion trajectory for electrified forklifts, the transition from ICE and lead-acid machines faces vital headwinds, comparable to:

Prime prematurely capital outlay: The preliminary funding for Li-ion forklifts and the needful charging infrastructure stays a number one barrier, particularly for budget-conscious SMEs.

Advanced infrastructure necessities: Probably the most important buyer friction level is electric infrastructure. Knowledge signifies 50-60% of charging installations require facility upgrades, which is able to upload as much as 25% to the whole challenge value.

Provide chain and experience gaps: Whilst making improvements to, the provision chain and after-sales marketplace for Li-ion parts don’t seem to be but as mature as the ones for ICE or lead-acid applied sciences.

Forklift electrification has handed the tipping level, evolving from a forward-looking development right into a core technique that determines long term undertaking competitiveness. Proactive leaders who actively undertake electrification are leveraging vital operational value benefits, enhanced sustainability credentials, and awesome provide chain resilience. Against this, enterprises that lag in the back of might face the twin pressures of value disadvantages and technological misalignment. As battery era continues to advance, lifecycle value benefits building up, and charging infrastructure turns into extra delicate, electrical forklifts are swiftly transitioning from a “most popular possibility” to the “default configuration” in international commercial and logistics sectors, redefining the long run panorama of subject material dealing with.

{kind=link}